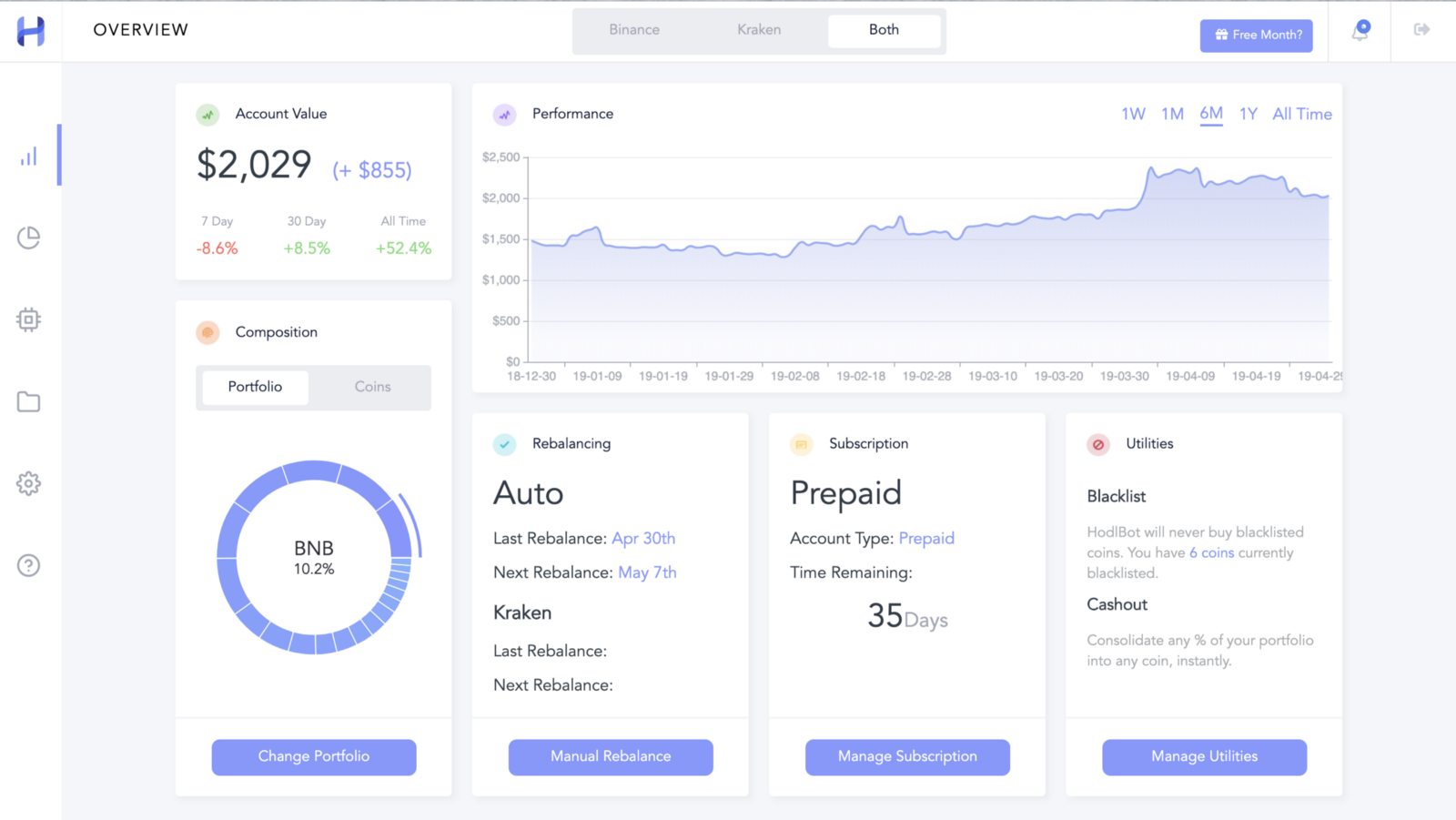

HodlBot is a customizable cryptocurrency trading bot that enables users to index the market, create custom portfolios, and automatically rebalance their cryptocurrency portfolios.

Grow your portfolio like the world's most sophisticated investors. We're making institutional portfolio management software available to everyone.

HodlBot is free to try for the first 7-days. A paid subscription starts at only $3/month.

Connect Exchange

Connect HodlBot to your exchange. API keys are securely encrypted (HMAC SHA-256).

Create or select strategy

Create a custom portfolio based on advanced metrics or implement an existing strategy.

Automatically Rebalance

HodlBot keeps your portfolio on track by automatically executing portfolio rebalances.

So you're new to HodlBot? No problem.

Pricing

HodlBot's pricing is tiered based on your portfolio size in order to keep our service affordable for those with smaller account sizes.

Diversification mitigates risk and improves returns. Studies found that 95% of active traders fail to beat the index. We built the HODL indices for users who want to diversify across the market instead of picking individual coins.

Create Portfolios with Advanced Market Metrics

Customized Portfolios

Select any coins, choose a weighting strategy, and see how it performed in the past. Use advanced market metrics to construct dynamic portfolios. You can also create a cryptocurrency index comprised of the top N coins.

Rebalances Keep Your Portfolio on Track.

Automatic Rebalancing

When the market shifts, a portfolio will drift away from its target allocation. HodlBot automatically rebalances your portfolio to keep it on track, saving you time. Portfolio rebalances generally lead to risk mitigation and improved returns.

Customize HodlBot to Fit your Preferences.

Tailored to Your Needs

Change your rebalancing frequency, blacklist coins you want to avoid trading, liquidate your assets anytime. HodlBot is highly customizable. On top of that, we provide 24/7 customer support.

How it Works

HodlBot simplifies the trading experience by making it possible to manage your portfolio without interfacing directly with exchanges.

Join Thousands of Happy Customers

Want to talk to active users? Join our 600+ member Telegram group.

Not bad for ~5 weeks! 🤙🏼😁

Bit over a month into using @hodl_bot and the portfolio I put together is up + 13.4%. The total market is up 6.8%, so its outperformed the global crypto market by 6.6%, or around 2x, since Feb 19.

Beau Stoner (@BeauStoner)

As the global pool of hashing power grows more liquid, arbitrageurs may see a financial incentive in "rent-a-miner" attacks, writes Anthony Xie of @hodl_bot. https://t.co/1fc5OMJstA

CoinDesk (@coindesk)

I've kept quiet about the #Binance SYS incident until now. Here's my take after analyzing a ton of the historical data from Binance's API. There's a lot of new information that no one has talked about before. https://t.co/pQUHWgH9jO

anthony xie (@XieToni)

In the stock market, I'm all about index funds. They perform well and the fees are low. I'd love something similar for cryptocurrency, and while options have started appearing, they are often pretty expensive. Hodlbot is different. Check it out: https://t.co/tVHdApHTWG #hodlbot

Mike Greiner (@mikegreiner)

@hodl_bot saves a ton of time & headaches. I have a new romance, thanks HodlBot. pic.twitter.com/rpSU1SBUM7

After winning $25, 000 at the #VelocityFundFinals and launching in April 2018, @UWVelocity company @hodl_bot has now traded over $25M in cryptocurrency and processed over 70,000 transactions. Read more about what HodlBot is up to here! https://t.co/DqgvoksTyp

Velocity (@UWVelocity)

After my experience w/a VPS & @Profit_Trailer - ended up nicknaming the bot "MyExWife", because all it did was cost me money.@hodl_bot is extremely easy to setup & a steal in comparison. Great way to get into crypto by passive-index-investing in the market as a whole 😍🙏🏽🔥👍🌕

Luis Hurtado (@LHurtado)

How cryptocurrency prices affect the number of HODL comments.https://t.co/KQ85t6P83O

Emin Gün Sirer (@el33th4xor)

"No one has any clue of what will happen to cryptocurrency prices in the short-term. But as a HODLER, we are confident that the price and value of cryptocurrencies will increase in the long run." @hodl_bot #bitcoin #Cryptotrader #BitcoinTwitter

Denounce with righteous indignation and dislike men who are beguiled

and demoralized by the charms pleasure moment so blinded desire that

they cannot foresee the pain and trouble.